On January 9th, 2026, Stellantis confirmed it will stop selling traditional plug-in hybrid versions of the Jeep Wrangler and Grand Cherokee (4xe) and the Chrysler Pacifica Hybrid in North America for the 2026 model year. Stellantis framed the move as a response to shifting customer demand and a pivot toward other electrified powertrains.

The immediate storyline is familiar to others seen in recent news: the EV market is cooling, and automakers are pivoting away from electrified models. However, there’s a more important signal for consideration. Plug-in hybrids (PHEVs) have increasingly been looked at as a near-term ‘bridge technology’, acting as an on-ramp to EVs for consumers and a way for automakers to maintain electrification momentum while the EV market works through pricing, charging, and policy uncertainty. But now that Stellantis, who is the current PHEV market leader (as of Q3 2025), is starting to back away from its most visible plug-in models, it could make the next phase of electrification more complex.

A small share of models, a large share of plug-in sales

Atlas EV Hub’s EV Market Dashboard shows that as of Q3 2025 there were 143 EV models on the market (BEVs + PHEVs), including 58 PHEV models. The three Stellantis PHEVs implicated by this January 9th announcement represent three models, or about two percent of all EV models available and five percent of all PHEV models.

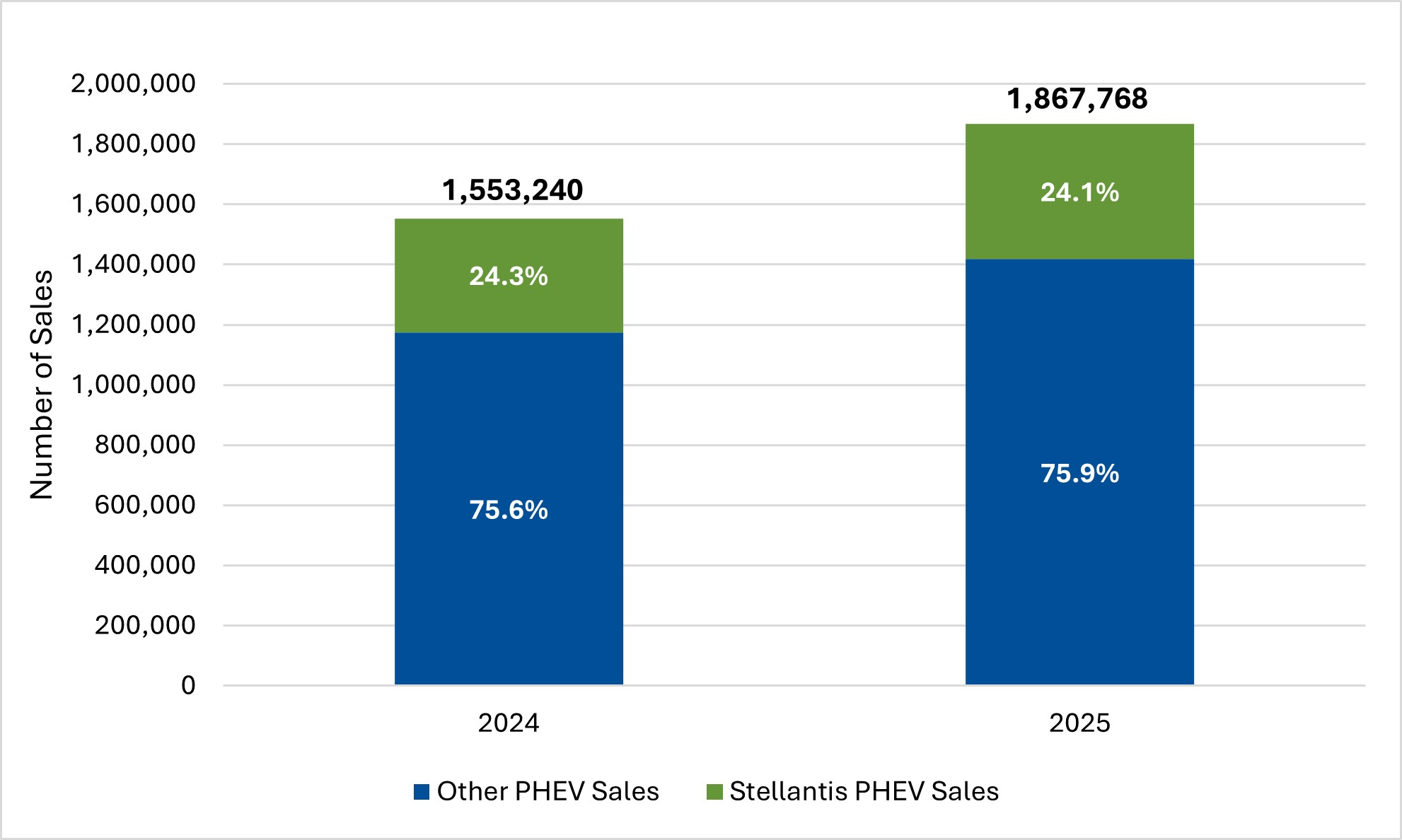

However, the PHEV market is very concentrated, and Stellantis has been a central driver of it. Between October 2024 and October 2025, cumulative U.S. PHEV registrations increased from 1.53 million to 1.87 million, or about 18 percent over the 12-month period. Over that same time period, Stellantis’ cumulative PHEV registrations rose from 378,000 to 450,000, an increase of around 17 percent. That means Stellantis accounted for roughly 23 percent of national PHEV growth year-over-year (YoY), with the three newly discontinued models driving nearly all of this growth (see Figure 1).

Figure 1. Stellantis Drove Nearly One Quarter of US PHEV Growth (Oct 2024 – Oct 2025)

Nearly all of Stellantis’ PHEV registrations come from Jeep and Chrysler models that are now being discontinued. Only about 1.5 percent come from other brands like Dodge or Alfa Romeo.

Source: EV Market Dashboard

Their market share is even clearer when you look at specific vehicle types. In PHEV minivans, Stellantis holds roughly 40 percent market share as of Q3 2025, well ahead of Honda at 24 percent and Toyota at 23 percent. When one of the few plug-in options in a practical, high-utility segment exits, the consumer impact can be larger than the initial math suggests because there are fewer comparable alternatives to absorb demand.

Stellantis’ shift matters, not because the market loses three models to choose from, but because those models sit inside a category where a small number of manufacturers account for a large share of plug-in adoption. As the EV market cools, losing momentum in the plug-in bridge category could make the transition feel less linear for consumers and planners.

The affordability constraints are still present

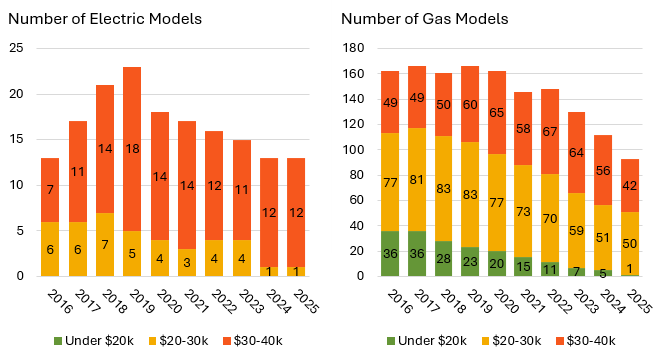

This shift also lands in the middle of a broader affordability trend. Atlas’ October 2025 issue brief, Affordable Vehicles in Decline, documents a multi-year contraction in affordable vehicle options (vehicles under $40K) and shows how the affordable end of the EV market has thinned as the overall product mix has tilted toward larger, higher-margin vehicles (see Figure 2). In that context, the exit of mainstream plug-in options is not just a product planning footnote. It reinforces a broader pattern: even when the EV market grows in total, the vehicle options that broaden adoption can be the first to disappear when manufacturers adjust strategy.

Figure 2. Number of Available Models Under $40,000 from 2016 – 2025, for EVs and Gasoline Vehicles

The Starting price for the newly discontinued Jeep Grand Cherokee 4xe, Wrangler 4xe, and Chrysler Pacifica PHEV models all had a starting price above $50,000 MSRP for the 2025 model year.

Source: Atlas analysis of fueleconomy.gov data.

The 2026 pipeline could address both availability and price

As the year progresses, the outlook may not be uniformly negative. Several 2026-era launches are positioned to expand the supply of lower-cost, mass-market EV options at the same time they broaden model availability in familiar segments. The next-generation Nissan LEAF, continued affordability pressure from the Chevrolet Equinox EV, and new entrants like the Rivian R2 and Slate Auto’s lower-cost truck concept are all aimed at capturing the sub-$50K vehicle market segment.

If these launches arrive on schedule and their advertised price points hold, they could help counteract two of the most persistent constraints in today’s market: a shrinking set of attainable models and a limited set of practical options for mainstream households. That will be big question as the year continues. Stellantis’ pullback makes the near-term bridge more uncertain, but a strong, affordable wave of new BEVs could widen the path again, addressing both choice and price in the same step. Atlas EV Hub will continue to update our EV Market Dashboard monthly with the latest sales data available and keep you updated on major EV news as it develops.